Structural adhesives are

those adhesives whose strength is important to the success of the assembly.

Increasing demand for reducing weight, reduce emissions, and increasing

efficiency has led to the incorporation of lightweight materials such as

aluminium and composites for fabricating components, has led to the increased

usage of structural adhesives. Structural adhesives offer several benefit to

fabricators and builders which includes improved product quality, improved

production speed, and reduce costs.

Sample PDF of this Report at http://www.marketsandmarkets.com/pdfdownload.asp?id=209974695

The global structural adhesives market is witnessing excellent growth with rising demand from the Asia-Pacific region, especially from China and India. The major demand for structural adhesives is expected to come from transportation industry especially from automotive, marine, aerospace, and bus & truck applications. Penetration of composites for fabrication of wind blades of longer blade length, wind towers and cover of gear boxes will increase the demand of structural adhesives in wind industry. The demand for structural adhesives is increasing due to rising demand for weight reduction, excellent mechanical performance, reducing manufacturing time and costs, and increasing penetration of composites.

Epoxy, polyurethane and methacrylate adhesives to register excellent growth

Epoxy adhesives are widely used

for bonding components, such as rotor blades of wind, car hoods and doors,

cockpits in aircrafts, engines, radomes, floorings, and fairings of aircrafts. Polyurethane structural adhesives are

extremely versatile and can form tougher bonds with excellent peel strength. The

demand for polyurethane adhesives is increasing due to the rising demand from structural

bonding for bonding of plastics, sheet molding compounds, and for cryogenic

applications. Methacrylate adhesives demand is driven by marine and

transportation industry.

DRIVERS FOR THE END-USER INDUSTRY

Sources: Press Releases, Expert

Interviews, and MarketsandMarkets Analysis

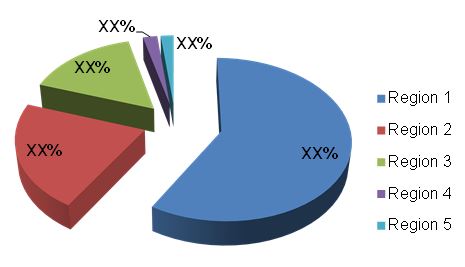

The demand for structural

adhesives is majorly from Asia-Pacific

Asia-Pacific accounts for the largest share of the total structural adhesive market, while European market is well established and in the maturity phase. The European structural adhesives market is estimated to witness a slower growth rate as compared to North America. The Asia-Pacific structural adhesives market is in a growth phase attributed to the booming aerospace, wind, automotive, and construction industries in China and India. The RoW structural adhesive market is also estimated to enter into the growth phase as construction activities are increasing at a high rate due to global events, driving the structural adhesives market.